Credit Card Marketers: Do you know what the CARD Act is ?

Apr 4, 2014

Affiliate Managers, Finance & Insurance

Most advertisers are aware that the Federal Trade Commission, and its Bureau of Consumer Protection, is the watchdog agency for deceptive and unfair advertising practices.

In the world of credit card marketing, however, there is a different federal organization charged specifically with oversight into deceptive credit card advertising practices. They use a fairly recent piece of legislation called the CARD Act that every marketer at a credit card company should know, cold.

Here are the cliff notes on the CARD Act, followed by tips for monitoring credit card ads for compliance

But wait, there's more! In October 2013, the CFPB announced it will try to expand the scope of products and services they monitor, beyond what is currently covered by the CARD Act. It released a list of marketing practices that will receive greater scrutiny, including:

But wait, there's more! In October 2013, the CFPB announced it will try to expand the scope of products and services they monitor, beyond what is currently covered by the CARD Act. It released a list of marketing practices that will receive greater scrutiny, including:

- The CARD Act stands for the Credit Card Accountability, Responsibility & Disclosure Act

- The new law was created by the Consumer Financial Protection Bureau (CFPB), a federal consumer watchdog that is less three years old

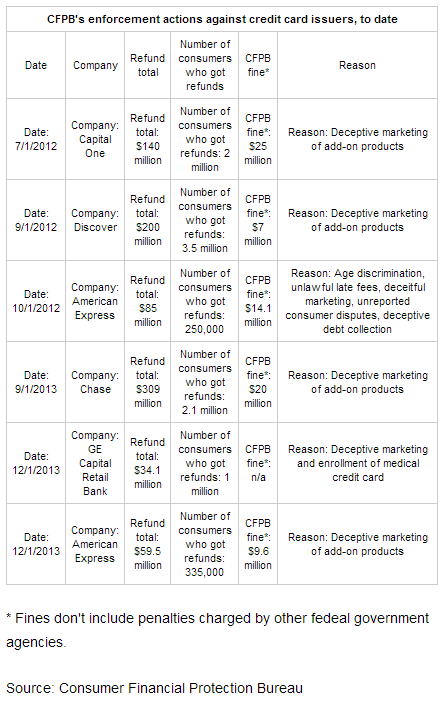

- The law has been used to fine credit card issuers more than $75 million. It has also ordered them to pay $827 million in refunds to more than 9 million consumers. All in less than 3 years!

But wait, there's more! In October 2013, the CFPB announced it will try to expand the scope of products and services they monitor, beyond what is currently covered by the CARD Act. It released a list of marketing practices that will receive greater scrutiny, including:

- Add-on Products: The CFPB is worried about how card issuers market their add-on products. In 2012, the Bureau fined Discover and Capital One $32 million for what they believed were deceptive marketing of their add-on products. In 2013, it fined Chase and American Express for the same reason

- Application Fees: The CFPB also wants to increase regulation on how much an issuer can charge for application fees. Currently, the CARD Act only governs a consumer’s first-year fees, not how much they pay to open an account.

- Disclosures on Minimum Payments: Issuers are currently required to include disclosure language on statements that educates consumers on how long it takes to pay off a balance when only the minimum required amount is paid. The CFPB reported that many consumers pay their bill online or via auto-deduction and do not see the statement disclosures. The Bureau will investigate other ways to deliver what it believes is vital consumer protection information

- Disclosures on Interest Payments: The CFPB also wants to make sure consumers are appropriately educated on how interest payments are calculated , especially for more complex topics like deferred interest rate cards or past-due interest charges.

- We find your offers: Monitor any online source where offers appear, including ads on search engines, contextual networks, emails, landing pages, and tweets. We also monitor display ads. Tell us the sites to monitor or let us find them for you. We monitor any content source necessary to track down offers and ensure regulatory compliance.

- We compare against rules: Ensure that offers comply with your pre-set rules for must-haves and can't-haves. Text is highlighted on-page and screenshotted for future use. ‘Failed’ content will be continuously re-checked until it is resolved. Changes are shown in the case management system.

- We help you contact offenders: Easily contact offenders and then verify that issues have been resolved